Financial Statements

The statements, prepared to know the result of the business and the financial position of the business, are called financial statements. The statement prepared for ascertain gross profit or loss is called Trading Account. The statement prepared to ascertain the net profit is called Profit and Loss Account. Trading and Profit and Loss Account taken together is called the Income Statement. Statement prepared to know the financial position of the business is called the Balance Sheet.

Objectives of Financial Statements

Following are the objectives of preparing financial statements:

1. Ascertain the result of business activities

One of the important objectives of preparing financial statements is to ascertain the Income. Financial statements provide information about the profit earned or loss incurred during a particular accounting period or year.

2. Ascertain the financial position of business

Balance Sheet provides information about the financial position of business on a particular date.

3. Correct decision making

Financial statements are helpful in decision making for the business on the basis of the information provided by financial statements, future decisions can be taken correctly.

4. Judging the performance of management

Financial statements are helpful in judging the performance of management and utilization of resources of a business house.

5. Ascertaining the cash position of business

The cash position indicated by the financial statements helps the business in planning the payment of cash to creditors, suppliers, etc.

Income Statement

Income statement is prepared to find out the profit or loss of business for a particular accounting year. Income statement is made up of the following accounts:

- Trading Account

- Profit and loss Account

Trading Account: Trading Account is prepared to find out the Gross profit earned or Gross loss suffered by the business from business activities during an accounting year. This account is prepared in T-form. Following is the proforma of a Trading Account:

Profit and Loss Account: After finding out the gross profit or gross loss by preparing the Trading Account, Profit and Loss Account is prepared to find out the net profit or net loss of the business during an accounting year. This account is also prepared in T-form. Following is the proforma of a Profit and loss Account:

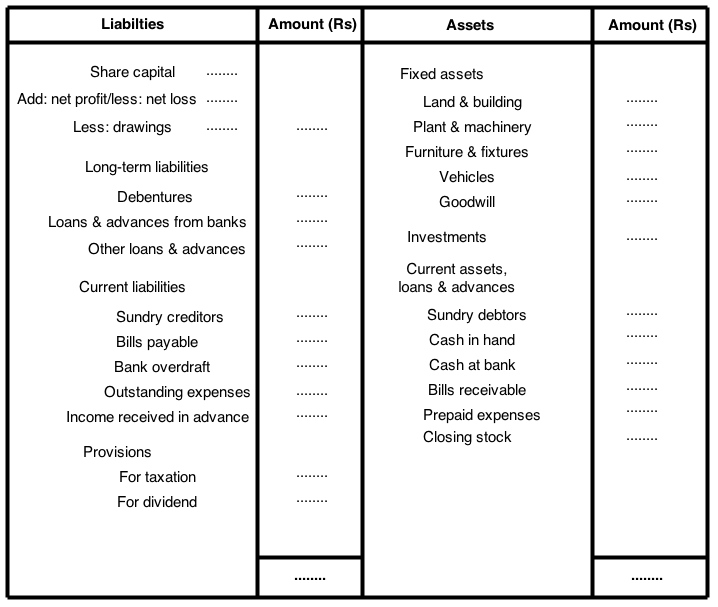

Balance Sheet

Balance Sheet or Position Statement is prepared to find out the financial position of a business on a particular date. Generally, it is prepared on the last date of an accounting year. It is prepared after preparing Trading Account and Profit & Loss Account.

Balance Sheet has two sides. Left hand side is known as Liabilities side and right hand side is known as Assets side.

Liabilities

The Liabilities side is used for showing liabilities of the business. The term liabilities include ‘Internal Liabilities’ and ‘External Liabilities’ of the business. Internal liabilities means the amount payable by the business to its owner, while external liabilities mean the amount payable to outsiders.

Assets

The Assets side is used for showing the assets of the business. The term assets includes fixed assets and current assets of the business.