Ledger

All transactions related to a head of account are recorded in different books. To know the total volume and value of transactions pertaining to a particular account these have to be brought at one place. The book in which all accounts are maintained is called Ledger. It contains the complete set of accounts for a business entity. The process of preparing necessary ledger accounts and transferring the information recorded in day books to these accounts according to accounting rules is called ledger posting.

Ledger is the principal Book of double entry accounting system.

Purpose of Ledger

1. Quick information about various transactions: Ledger sets the relationship between the business enterprise and business transactions with the help of an account.

2. Proper control over transactions: Separate ledger accounts are maintained for each type of transaction.

3. Helpful in preparing Trial Balance: The final balances of all ledger accounts are shown in the Trial balance, which helps in ensuring that books are arithmetically correct.

4. Helpful in preparing Financial Statements: The financial statements of a business concern are prepared with the help of trial balance which in turn is prepared on the basis of the balance of different ledger accounts.

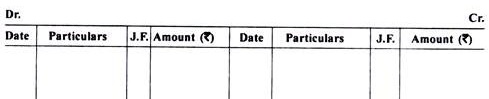

Format of Ledger Account

Ledger account is prepared in T shape, which is divided into two parts. Left side is known as Debit side and right side is known as Credit side.

The following information is recorded in the various columns on both sides of a ledger account:

Date: In this column, the date of a transaction is recorded.

Particulars: In this column the details of the transaction is recorded, on the debit side, the word ‘To’ and on credit side, the word ‘By’ are prefixed.

Journal Folio (J.F.): In this column the page number of book of original entry is recorded.

Amount: The Amount of the transaction is recorded in this column.